Market research of the European real estate market.

Comparative analysis with the markets of Southeast Asia and the Middle East

2025

Summary

- Introduction: An overview of the European luxury real estate market and its place in the global economy.

- Market size and dynamics: Detailed analysis of market size and growth rates both in Europe and in comparable markets (Turkey, Cyprus, Dubai, Southeast Asia). Key figures for 2022-2025 and future forecasts are included.

- Luxury real estate in Europe: Study of market peculiarities, investment attractiveness of Cyprus and Turkey as key regions on the EU periphery.

- Comparison with Southeast Asian markets: Analysis of affordability, investment attractiveness and key market drivers in SE Asia.

- Demand Geography and Preferences: Study of buyers’ backgrounds, motivations and preferences by property type.

- Price ranges of elite real estate: Comparative analysis of prices per square meter in different regions.

- Investment Outlook and Risks: Overview of macroeconomic, geopolitical, regulatory risks and opportunities for investors.

- Recommendations for investors: Practical advice depending on the preferred investment strategy (conservative, balanced, aggressive).

- Conclusions: Summary of the research findings and market forecast for 2025-2030.

Introduction

The European real estate market has traditionally attracted wealthy buyers from all over the world due to its unique combination of historical heritage, stability and high quality of life. This study considers both traditional European markets and promising destinations outside Western Europe – Turkey, Cyprus, Bali, Thailand and Dubai.

The analysis covers the size and dynamics of these markets, the portrait of demand from high net worth individuals, preferred property types, price ranges, as well as influencing legislative factors, risks and opportunities for investors.

Elite real estate” usually means the most expensive 5-10% of objects – luxury villas, penthouses, mansions and apartments in prestigious locations.

1. volume and dynamics of the real estate market

Global and European trends

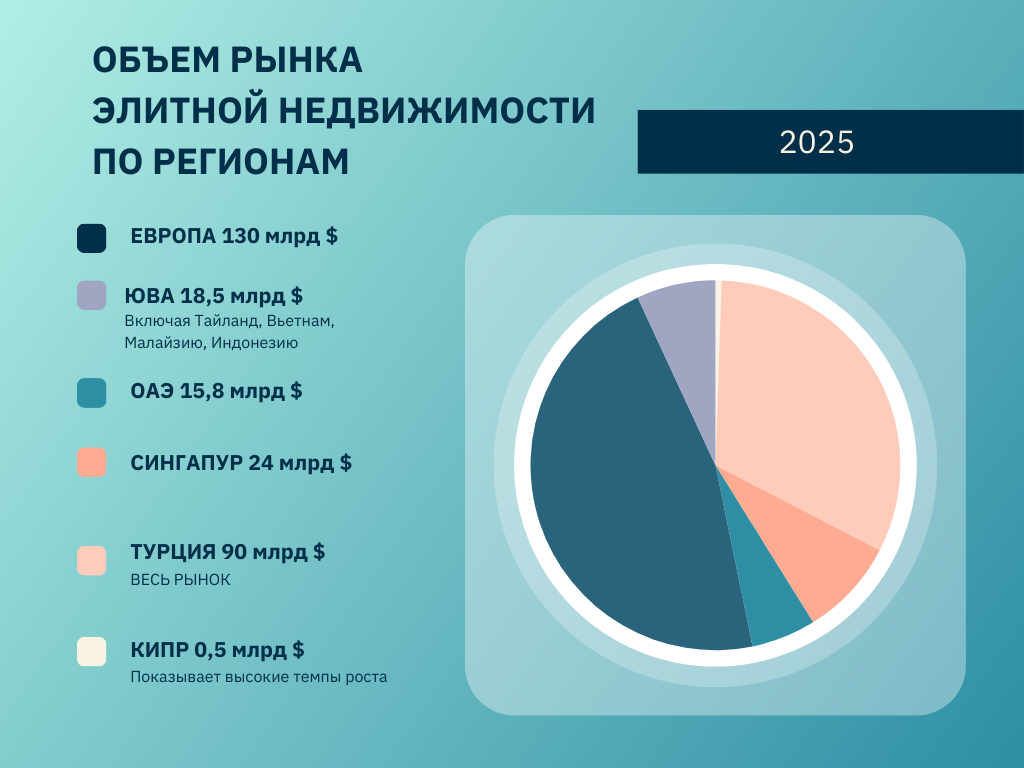

The total volume of the global luxury residential real estate market is estimated at approximately $290 bln by 2023. The European segment occupies a significant share: the total volume of the luxury residential real estate market in Europe in 2025 reaches ~120 billion euros. Over the past three years, the European luxury segment has been growing at a moderate rate of around 4% per annum, and is forecast to further increase to ~€147bn by 2030.

Moderate growth in Europe is explained by post-pandemic recovery and expected monetary policy easing (interest rate cuts in 2024-2025). Nevertheless, the dynamics differ across countries: some markets in Western Europe are stagnating, while some countries have recorded growth due to foreign capital inflows.

The European real estate market remains the largest in the world with a volume of about $1.95 trillion. It is expected to reach $2.43 trillion by 2029 at an average annual growth rate of 4.5%.

Fast-growing markets outside Europe

Luxury real estate is booming in a number of alternative destinations. Dubai stands out in particular: over the past two years, there has been an explosive growth in demand. In 2023, 431 transactions worth over $10 million were made in Dubai – a record high, 80% more than in the next largest market (London).

Dubai’s rapid growth is due to zero taxes, ease of doing business and the influx of rich migrants (from Russia, Asia, Europe). Since 2020, luxury housing prices in Dubai have more than doubled; by the end of 2024, the average price of prime properties reached ~Dh3,700/ft² (≈€9,000/m²) with an annual growth rate of ~7%.

Turkey is also showing impressive dynamics: in 2022, it ranked 1st in the world in terms of housing price growth – +41.7% over the year. This is due to both strong domestic demand amid inflation and an influx of foreign investors. Turkey’s total real estate market reached ~$90bn in 2023, and is forecast to grow to $150bn by 2028 (average annual growth of ~11%).

In Indonesia, the island of Bali has experienced a meteoric rise after the pandemic downturn: in 2023, the number of real estate transactions in Bali increased by 40% compared to 2022, while prices rose by an average of 15%. In Thailand, the luxury segment is also recovering, with prime property prices up 6% year-on-year in 2023, reflecting the return of overseas buyers.

At the same time, the Cyprus market is generally stable (total transaction volume of ~€5.5bn in 2023, the same as in 2022), but the ultra-expensive housing segment there has sagged after the closure of the “golden passport” program – in 2023 there were only 164 transactions over €1.5m (-26% vs. 2022), worth about €440m (only ~8% of the market volume).

| Market | Estimated volume of the luxury market | Dynamics of the last years | Forecast for 3-5 years |

|---|---|---|---|

| Europe (cumulative) | ~€120 bln (2025) | ~+4%/year (2020-2025) | ~€147 bln by 2030 (≈+4%/year) |

| Dubai, UAE | ~$15.8 billion (2025) | >2× price growth from 2020; $10M+ deals boom | $22.9 bln by 2030 (+7.7%/year) |

| Turkey (all real estate) | ~$90 bln (2023) | +41.7% q/q price growth (2022) | $150 bln by 2028 (+11%/yr) |

| Thailand (prime segment) | ~$3.4 billion (2024) | ~+6% price growth (2023) | $4.0 bln by 2029 (+3.4%/year) |

| Cyprus (≥€1.5 million) | ~€0.44 bln (2023) | -26% of transaction volume (2023 vs 2022) | Demand is expected to recover |

| Bali, Indonesia | (no exact data available) | +15% price growth, +40% transactions (2023) | Steady growth with tourism (10%/year+) |

Sources: market statistics, analytical reports, 2023-2025

2. luxury real estate in Europe: key markets

2.1. Cyprus: market peculiarities and investment attractiveness

The luxury real estate market in Cyprus is characterized by the following features:

- Average cost of luxury real estate: 6 500 €/м²

- Rental yield: 4.5%

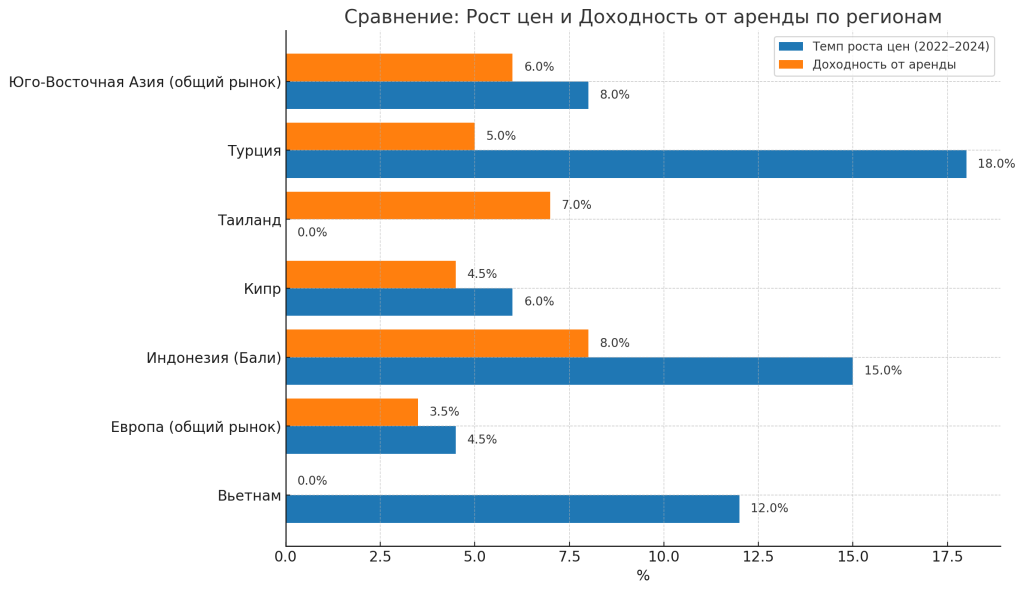

- Price growth rate (2022-2024): 6%

- High investment attractiveness

- Average level of political stability

Key factors affecting the Cyprus real estate market:

- Residence through Investment Program (requires purchase of real estate worth €300,000 or more)

- Favorable tax treatment

- High tourist attraction of the island

- The political situation surrounding the division of the island

In 2024, real estate sales in Cyprus increased by 30% compared to the previous year, the average value of properties is 230,000 €. Apartments are bought twice as often as houses. At the same time, there is a slowdown in price growth to 5.6% in 2024 compared to 7.7% a year earlier.

As of March 2025, the average price of an apartment in Cyprus is €504,000, with an average price per square meter of €4,000. A rental yield of up to 10% makes Cyprus one of the leaders in this indicator in the EU countries.

2.2. Turkey: market peculiarities and investment attractiveness

The luxury real estate market in Turkey is characterized by the following indicators:

- Average cost of luxury real estate: 3 500 €/м²

- Rental yield: 5%

- Price growth rate (2022-2024): 18%

- Average investment attractiveness

- Low level of political stability

The main factors affecting the real estate market in Turkey:

- High inflation (reached 85% in October 2022, reduced to 47% by the end of 2024)

- Depreciation of the Turkish lira (from 29.4 to 35.1 lira per dollar during 2024)

- Citizenship by Investment Program (requires purchase of real estate worth $400,000 or more)

- Geopolitical risks

In 2024, 1,478,025 residential properties were sold in Turkey, an increase of 20.6% compared to 2023. A total of 23,781 residential properties were sold to foreigners, with the highest number of sales to foreigners in Istanbul (8,416 properties) and Antalya (8,223 properties).

In 2025, the real estate market in Turkey is expecting record sales growth. Expert forecasts point to possible sales exceeding 1.5 million units, which would surpass the 2013 record of 1.4 million.

3. Comparative analysis with Southeast Asian markets

3.1. Overview of key countries

| Country | Market volume ($ bln) | Price growth rate (%) | Rental yield (%) | Cost of luxury real estate (€/m²) |

|---|---|---|---|---|

| Singapore | 240 | 7.5 | 3.8 | 25,000 |

| Thailand | 120 | 6.5 | 7.0 | 7,000 |

| Vietnam | 65 | 12.0 | 6.5 | 4,500 |

| Indonesia (Bali) | 40 | 15.0 | 8.0 | 3,800 |

| Malaysia | 50 | 4.0 | 5.0 | 3,200 |

The real estate market in Southeast Asia shows high growth potential due to the region’s rapid economic development, urbanization and growing middle class. Singapore, Thailand and Vietnam are particularly attractive for investors.

3.2. The cost of luxury real estate

The European luxury real estate market is characterized by higher prices (average 10,000 €/m²) compared to Southeast Asia (average 5,000 €/m²). The exception is Singapore, where the cost of luxury real estate can reach 25,000 €/m².

In Cyprus, the average cost of luxury real estate (6,500 €/m²) is comparable to Thailand (7,000 €/m²), but significantly higher than in Malaysia (3,200 €/m²) or Indonesia (3,800 €/m²).

Turkey offers the most affordable luxury real estate among the considered European countries (3 500 €/m²), which makes it attractive for investors with a limited budget.

Southeast Asian countries have higher price growth rates and rental yields than European countries, making them attractive to investors focused on high yields. However, European markets offer greater stability and lower risks.

Investment indicators

4. Customer preferences and geography of demand

4.1. Portrait of demand from affluent individuals (HNWI/UHNWI)

The luxury real estate segment is becoming increasingly global: the richest people of the planet are actively diversifying their investments across different countries. Western European cities (London, Paris, Zurich, Geneva, etc.) have traditionally been among the leaders in attracting HNWI capital due to their economic and political stability.

For example, London has historically been a magnet for the ultra-rich from CIS countries, the Middle East, China, India, etc., but in 2022-2023, a new trend was observed – the influx of wealthy Americans to Europe against the backdrop of a stronger dollar. Wealthy American buyers actively bought real estate in the UK, France, Italy and Portugal, taking advantage of the exchange rate difference and attractive prices in euros.

Geopolitical events significantly affected the structure of demand. After 2022, many rich Russians and Belarusians were forced to reorient from Europe to alternative markets. Dubai became one of the main destinations for capital from the CIS: the emirate did not join the sanctions and offers comfortable living conditions. As a result, the share of Russians among buyers of luxury real estate in Dubai has grown dramatically.

In addition, Russians are actively investing in Turkey, both to save money and to obtain citizenship. In 2022, Russian citizens became the largest group of foreign buyers of housing in Turkey, although by 2023 their activity slightly decreased due to currency and sanctions restrictions.

4.2. Preferences by property type

The tastes of buyers of luxury real estate strongly depend on the location and purpose of purchase. In megacities (London, Paris, Dubai, New York, etc.), the greatest demand is for penthouses and apartments in new premium-class residential complexes, often with “5-star” service (concierge, SPA, 24/7 security).

Villas prevail in the resort regions of Europe: on the Côte d’Azur these are historical mansions in the style of “belle epoque” and modern villas with swimming pools in Saint-Tropez, Cap Ferrat, Cannes; in Tuscany – country estates with vineyards; in Ibiza and Mallorca – snow-white modern villas overlooking the sea.

In Greece and Cyprus, coastal villas in protected complexes are popular (for example, areas of Limassol with access to the beach or villas in Mykonos with a panorama of the Aegean Sea). In Turkey, foreigners prefer villas in Antalya, Alanya, Fethiye, and for the super-rich unique objects are available – historical mansions on the Bosphorus in Istanbul.

Bali and Phuket are almost exclusively villas: spacious Balinese-style houses with thatched roofs, gardens and swimming pools, or ultra-modern “infinity pool” villas on the hills overlooking the ocean. The apartment format is less relevant there (there are few high-rise condominiums), so luxury investors prefer to buy land and buildings.

4.3. Customer Motivations

- Investment and capital preservation is the key motive in most cases. Luxury real estate is seen by HNWI as a reliable asset and protection against inflation, especially in turbulent financial markets.

- Immigration benefits – Golden Visa and citizenship programs encouraged purchases in Portugal, Greece, Cyprus, Turkey, etc.

- Prestige and lifestyle – owning a penthouse overlooking the Burj Khalifa in Dubai or a villa on the Cote d’Azur in France emphasizes the status of the owner.

- Tax breaks – wealthy retirees from the US and South Africa have been moving to Portugal thanks to the NHR regime (tax-free pension for 10 years), while millionaires from France and Italy are relocating to Dubai and Switzerland to escape high taxes at home.

5. Price ranges of elite real estate (€/m²)

The cost of luxury housing varies extremely widely depending on the city/region. Below are the approximate price ranges per square meter in the main locations of the luxury market (for prime properties):

| Location | Typical prices of luxury real estate, €/m² |

|---|---|

| Monaco (Monte Carlo) | ~50,000 € on average; top new builds up to 100,000 € |

| London (UK) | 20,000-40,000 € (central areas of Mayfair, Knightsbridge, etc.) |

| Paris (France) | 15,000-25,000 € (8th, 6th arrondissement; best views of the Eiffel Tower are more expensive) |

| Madrid, Barcelona (Spain) | 8 000-12 000 € |

| Rome, Milan (Italy) | 8 000-15 000 € |

| Lisbon (Portugal) | 6 000-10 000 € |

| Athens/Greece | 4 000-6 000 €, villas in Mykonos ~8 000 € |

| Cyprus (Limassol) | 4 000-5 500 €/m², new on the coast – 8 000-10 000 €/m² |

| Istanbul (Turkey) | ~1,800 €/m² (luxury apartments), villas on the Bosphorus up to 5,000 €/m² |

| Bodrum/Antalya (Turkey) | 3 000-5 000 €/м² |

| Dubai (UAE) | ~9 000 €/m² (prime market), top penthouses up to 15 000 €/m² |

| Bangkok (Thailand) | ~7 000 €/m² (up to 10 000 € – super luxury) |

| Phuket (Thailand) | 4 000-6 000 €/м² |

| Bali (Indonesia) | 1 500-3 000 €/м² |

Sources: market analysis, real estate agency data, 2023-2025

6. Risks and opportunities for investors

6.1. Market risks

The elite real estate market in 2025 shows a mixed picture – it has faced a number of external and internal challenges, but on the whole remains stable and adaptive. Among the key risks for the coming years, experts note:

- Macroeconomic factors: rising interest rates and tighter credit conditions may narrow the pool of buyers, even though HNWIs are less dependent on mortgages. A global recession or a decline in the wealth of the top 1% will directly hit the demand for luxury real estate.

- Geopolitics: sanctions and instability affect capital flows. Sanctions restrictions for certain nationalities redistribute demand to other regions, which can lead to localized overheating.

- Regulatory changes: curtailing “investment” residence permit/citizenship programs deprives the market of part of the money inflow. In addition, there may be new restrictions, such as taxes on vacant housing or stricter checks on sources of funds.

- Excess supply: in pursuit of high prices, some markets risk building excessive volumes of luxury housing. For example, in Dubai there are periodic fears of “overheating” – if the pace of construction of ultra-luxury skyscrapers exceeds the real effective demand, it may lead to price adjustments.

6.2. Long-term opportunities and trends

- Sustainable development (ESG) and green architecture: Environmental friendliness and energy efficiency are coming to the forefront even in the luxury segment. Developers of luxury new buildings now initially lay down BREEAM and LEED certifications, install solar panels, recuperation systems, charging systems for electric cars, etc.

- Smart technology: the Smart Home has virtually become the standard: remote control of lighting, climate, multimedia, sensors and monitoring – affluent customers expect it by default.

- Locations in harmony with nature: Since the pandemic, HNWI interest in homes that provide privacy and contact with nature has increased.

- New Buyer Groups: In the next 5-10 years, the number of millionaires in the emerging economies of Asia, the Middle East, and Africa is expected to grow significantly.

- Diversification and services: The luxury market is becoming more service-oriented. Companies offering full-cycle services are growing: from selection and sale to property management, leasing, concierge services for owners.

Despite short-term challenges, luxury real estate continues to be a reliable investment asset for the richest people on the planet. The outlook for the next 3-5 years is for a moderate increase in activity as it adapts to the new realities and the post-pandemic economic recovery continues.

7. Practical recommendations for investors

📈 Conservative strategy

It is recommended to invest in real estate in Europe (including Cyprus) and Singapore, where political stability and legal protection of investments compensate for lower returns.

Suitable for: investors who value safety of capital above high returns; pre-retirement and retirement age; those looking for a “safe haven” for capital.

⚖️ Balanced strategy

It is recommended to diversify investments between European countries (Cyprus) and SEA countries with high political stability (Thailand, Malaysia).

Suitable for: middle-aged investors; those seeking a balance between return and risk; those who plan for both rental income and the possibility of personal use of the property.

🌐 Immigration strategy

To obtain residence permit or citizenship through investment, it is recommended to consider Cyprus (residence permit from €300,000) or Turkey (citizenship from $400,000).

Suitable for: those seeking a second citizenship or residence permit; those planning a family relocation; investors for whom immigration benefits are more important than purely financial returns.

🚀 Aggressive strategy

It is recommended to invest in countries with high rates of price growth and rental yields (Turkey, Indonesia, Vietnam), given the increased risks.

Suitable for: young investors with a high risk tolerance; those who have the ability to actively manage their investments; those who are ready for quick entry and exit from the market.

Conclusions

- The European luxury real estate market remains the largest and most stable in the world with a volume of around €120 billion in 2025 and moderate growth of around 4% per year. However, the dynamics vary significantly between countries and regions.

- Markets outside of Europe, especially Dubai and Turkey, are showing higher growth rates and rental yields, attracting investors focused on aggressive capital growth.

- Buyer preferences are evolving: there is a growing demand for environmentally friendly and technological properties, as well as for locations that provide privacy and proximity to nature.

- Geopolitical events and legislative changes (especially the abolition of “golden passport” programs) significantly affect the redistribution of investment flows in the global real estate market.

- For successful investment, it is important not only to analyze financial performance and growth rates, but also to take into account the specifics of legislation, taxation and political risks in each particular country.

Despite all the challenges, luxury real estate continues to be one of the most stable and attractive asset classes for wealthy investors. It is important to choose properties that match both your financial goals and personal preferences, and to carefully diversify your investments across different regions and property types.

© 2025 Market research of the European real estate market

All data are current at the time of publication. When using materials, reference to the source is obligatory.

Follow us on social media